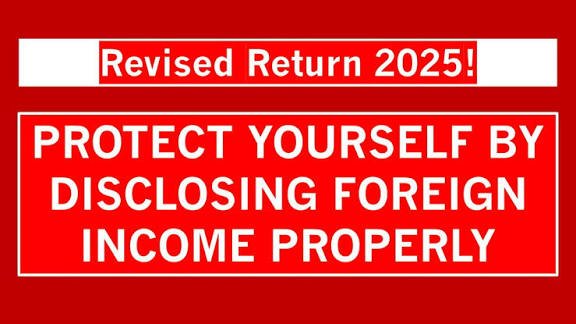

Missed Disclosing Foreign Assets in Your ITR? Revise Now Before Dec 31, 2025 to Avoid ₹10 Lakh Penalty & Legal Heat

If you missed disclosing foreign assets in the original ITR filings for the relevant assessment year must submit a revised return by December 31, 2025, to avoid a hefty penalty of ₹10 lakh and potential legal action under the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 [1].

To revise your ITR, you need to file an updated return (ITR-U) on the official Income Tax Department e-filing portal before the specified deadline.

Key Details:

Why revise?

Unreported foreign assets can trigger penalties under the Black Money Act (up to ₹10 lakh) and even prosecution (up to 7 years imprisonment) .

Non‑disclosure also revoke your right to claim DTAA benefits .

When to act:

Deadline: Revised/belated return must be filed by 31 Dec 2025 to avoid penalties .

How to disclose:

Fill Schedule FA (Foreign Assets) with country name, asset type, value in foreign currency & INR, opening/closing balances, etc.

Use ITR‑2/ITR‑3 (not ITR‑1/ITR‑4) .

What’s covered:

Bank accounts, stocks, real estate, mutual funds, trusts, custodial accounts, any foreign financial interest.

Even dormant accounts or minor holdings must be reported .

Penalties & Risks:

₹10 lakh fine for non‑disclosure (exemption only if total bank balance ≤ ₹5 lakh) .

Possible tax audit, scrutiny, and loss of DTAA relief .

Steps to file a revised return:

1. Gather all foreign asset docs (statements, acquisition dates).

2. Log into the Income Tax portal → “e‑File” → “File Revised Return”.

3. Complete Schedule FA, FSI (foreign income), and TR (tax relief) as needed.

4. Submit with DSC/EVC.

Team: Economiclawspractice.com